Finding the right health insurance plans for your clients is crucial in ensuring that hardworking individuals, families, and businesses can access quality healthcare without incurring exorbitant or unexpected out-of-pocket costs. As a broker or third-party administrator (TPA), it’s your responsibility to effectively articulate and distinguish the advantages and disadvantages of various health insurance plans that may suit your clients.

For instance, when it comes to self-funded health insurance, pros and cons lists can be beneficial tools for outlining how these plans function on the ground. This preliminary discussion process will help your clients move through the complex array of available offerings, empowering them to choose the plan best suited to meet their unique needs that will serve them for years to come.

Your Guide to Discussing Health Insurance Plan Advantages with Clients

When discussing plan advantages with your clients, you’ll want to be as thorough and detailed as possible. Below are a few of the most essential concepts and points you’ll want to highlight during these extensive conversations.

Practicing Clear Communication

Considering that most of your clients will be working outside the healthcare sector, they’ll likely be experiencing some stress at the thought of sifting through complicated layers of legal and medical jargon implicit in the decision-making process. To articulate plan advantages effectively, use clear language and even visual aids to explain key terms and concepts in simple terms.

Tailoring Plans to Meet Unique Needs

Matching health insurance plans to meet your client’s unique needs is arguably the most critical part of the conversation around plan advantages, considering that these advantages are only relevant insofar as your client can use them appropriately.

This highly tailored and detail-oriented part of the process involves learning the specificities of your client’s unique healthcare requirements; some of these aspects include discussing their available budgets or financial constraints, the size of their business or staff, their provider preferences, and more.

Emphasizing Quality Coverage

One of the most fundamental advantages of health insurance is comprehensive coverage for medical expenses that can arrive without warning. Clients should be aware of what their health insurance plan will typically cover and the type of care they’ll be receiving in exchange for their premiums. Explain that coverage may include hospitalizations, doctor visits, specialist consultations, prescription drugs, preventive care, and sometimes mental health services.

Incorporating Access to Preventive and Emergency Care

Emphasizing the value of preventive and emergency care will help your clients understand how important it is to have a holistic and comprehensive insurance plan. Complete protection begins with ongoing preventative care, including regular check-ups, screenings, and vaccinations; explain how insurance can provide clients with this proactive asset with little to no out-of-pocket costs.

However, when health crises arise, emergency care coverage intercedes in the event of accidents or sudden illnesses. Explain that insurance plans for such emergencies safeguard against unreasonable hospital bills or the possibility of treatment being delayed by financial complications.

Asserting Financial Security

Explain to your clients that comprehensive health insurance acts as a safety net that protects against high medical expenses, safeguarding their savings and financial stability. Consider sharing real-life examples and/or statistics demonstrating how medical bills can devastate one’s finances without proper coverage.

Reviewing Available Benefits

Alongside the more standard types of coverage detailed above, many clients will search for ancillary plans and products that provide them with even more excellent protection and peace of mind. Health In Tech now offers benefits such as Critical Illness, Accident, Dental, Vision, Term Life, and Gap coverage, all offset additional complexities and expenses for policyholders.

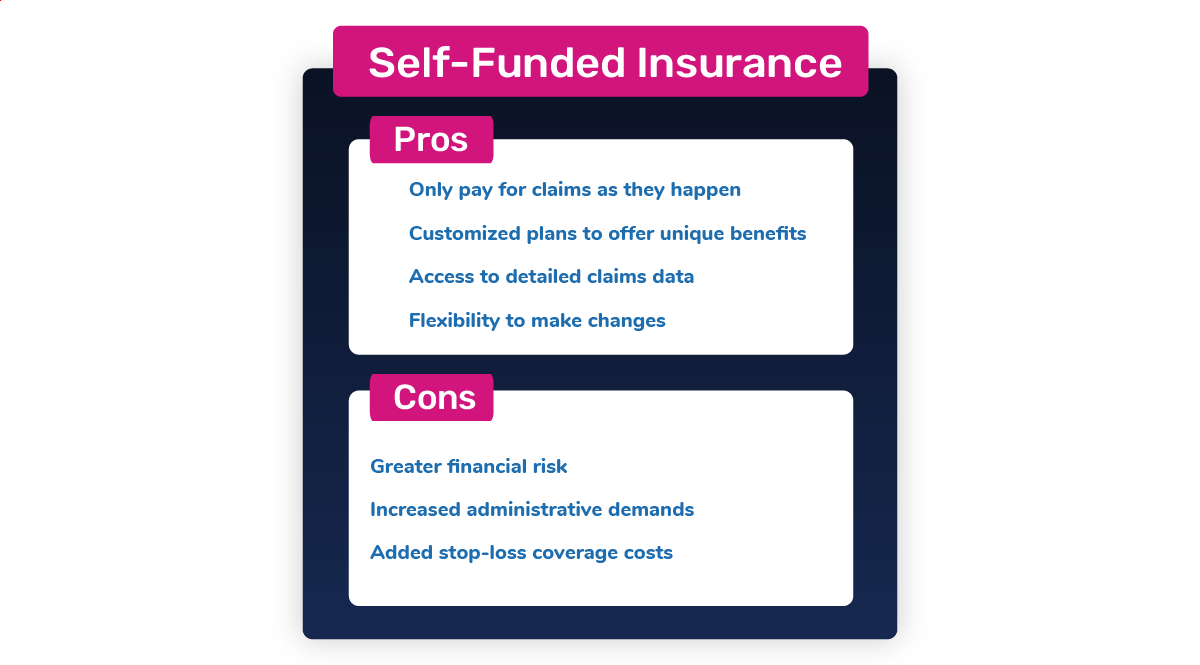

Explaining Self-Funded Health Insurance Pros and Cons to Clients

Helping your clients learn how self-funded health plans work is incredibly important, given that many businesses are turning to these solutions as flexible, cost-effective alternatives to traditional plans. Below are some self-funded health insurance pros and cons to explore with clients.

The Pros of Self-Funded Health Insurance

Regarding self-funded health insurance pros and cons, the benefits of self-funded plans far outweigh the drawbacks. For example, when an employer takes on some (or all) of the benefits claims costs, they’re given greater control over their healthcare costs.

By paying claims directly, employers avoid the profit margins of traditional insurance carriers, often resulting in lower overall costs for the company. Self-funded plans also help reduce costs because they usually avoid premium taxes imposed by state regulations, and employers can retain unused premiums if claims are lower than anticipated.

Moreover, self-funded plans provide transparency, as employers can see precisely where their healthcare dollars are going. Transparency is one of the most essential assets in the healthcare industry today, and self-funded plans help eliminate billing and compensation complexities. This transformative level of visibility enables better financial management and decision-making.

Flexibility is also a significant benefit to self-funded healthcare, allowing for high-caliber customization tailored to meet the specific needs of an employer’s workforce. In just two minutes, our eDIYBS system can generate proposals for your clients with 12 different plans and 4 tier rates, allowing you to quote, bind, and enroll groups easily.

The Cons of Self-Funded Health Insurance

Luckily, many of the apparent cons of self-funded health insurance are actually avoidable mistakes and misconceptions that can be easily circumvented through research and sufficient planning.

For instance, if clients are worried about assuming more significant financial risk with self-funded plans, explain that employers can better cushion themselves against month-to-month fluctuation by accounting for variable claims. Stop-loss insurance allows for further risk mitigation against unexpected catastrophic claims.

Some assume that navigating the legal and compliance challenges of self-funded plans may be burdensome because such plans must adhere to federal and state regulations. However, this can be avoided by building periodic claims audits into a business’ functional agenda or hiring a skilled TPA to handle day-to-day plan implementation.

Others believe that self-funded plans only make sense for larger companies. But small businesses can also save ample time and money by investing in these plans; at Health In Tech, we only require five employees to enroll in our eDIYBS system, making client eligibility more streamlined and autonomous.

Discovering the Self-Funded Health Insurance Pros and Cons with Health In Tech

After helping your clients understand self-funded health insurance pros and cons alongside other plan advantages and offerings, you’ll want to help them select or design a cradle-to-grave health insurance solution best suited to meet their needs.

Here at Health In Tech, we proudly support brokers, TPAs, employers, insurers, and members as they discover how they can make the most of their plan advantages, leveraging our tools and technology to create top-tier solutions that have successfully disrupted the norm in healthcare for over 30 years. Get in touch today to learn what Health In Tech can do for you and your clients.